Spotlight 63A: HMRC Doubles Down on Hybrid Property Structures

When HMRC first issued Spotlight 63 in 2023, it sent a clear warning to landlords using hybrid partnership structures. By the time we revisited the topic in 2025, many were already dealing with enquiries, uncertainty and, in some cases, significant tax exposure.

Fast forward to April 2026, and HMRC has gone further.

Spotlight 63A is not a new warning – it is a deliberate escalation. HMRC has now set out, in detail, exactly why these arrangements fail and made it clear that the issue has not gone away. If anything, the position has hardened.

For landlords who believed the risks had settled or were reassured that their structure was compliant, this latest update is a clear signal. HMRC is not revisiting this area; the aim is to significantly restrict its viability.

A quick recap: what Spotlight 63 was really about

At its core, Spotlight 63 targeted hybrid partnership arrangements used by landlords to reduce their tax liabilities.

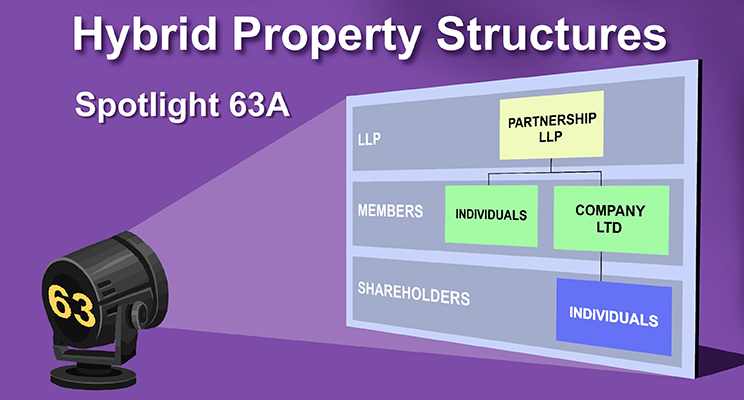

Typically, these structures involved a Limited Liability Partnership (LLP) with a corporate member. Rental profits could then be allocated to the company, allowing landlords to benefit from lower corporation tax rates rather than higher or additional income tax rates.

The growth in these arrangements followed the restriction of mortgage interest relief. For many leveraged landlords, the increase in tax liabilities created a strong incentive to find alternative structures.

As we highlighted previously, the issue was never simply the use of an LLP or a company. It was the disconnect between the legal form and the economic reality. Where profits were redirected without any genuine shift in control or risk, HMRC made it clear it would look through the structure.

What’s changed with Spotlight 63A

The key difference with Spotlight 63A is precision.

HMRC is no longer describing a risk in general terms. It is setting out how these arrangements are being marketed today and why they fail under multiple, overlapping pieces of legislation.

A common variation now involves indemnities. This is where the corporate member is said to assume responsibility for mortgage liabilities, creating what is presented as a capital contribution to the LLP, then used to justify allocating profits to the company.

HMRC’s position is that this is not a genuine capital contribution. As a result, the foundation for allocating profits to the corporate member falls away.

More importantly, HMRC is not relying on a single argument. It has identified several independent routes to challenge these structures:

- The mixed-member partnership rules (ITA 2005, ss.850C–850D) can reallocate excess profits back to the individual landlord

- Transferred income rules (ITA 2007, s.809AAZA) can treat income as still belonging to the landlord, regardless of the structure

- CGT transparency rules (TCGA 1992, s.59A) mean there is no effective transfer of the underlying property

- SDLT provisions can trigger charges on transfers and changes in profit shares

- In some cases, ATED may apply to high-value residential property held through corporate structures

The practical implication is clear: even if one argument were challenged, others remain. This is no longer a single-point failure; it is a structure HMRC can attack from multiple directions.

Why has HMRC issued this update now?

Spotlight 63A tells us something simple yet important: these arrangements are still in use.

Despite the original warning, promoters have continued to adapt and market variations of hybrid structures, often adding layers of complexity to address earlier concerns. For landlords under ongoing tax pressure, these solutions can still appear credible.

HMRC’s response is to remove any remaining ambiguity. This isn’t about raising concerns anymore; it’s about dismantling the structure, point by point.

More broadly, this reflects a shift in HMRC’s approach in many areas of taxation and the use of reliefs. Rather than issuing high-level warnings, it is increasingly setting out detailed legislative reasoning. The message is not just that a scheme is risky – it is that HMRC already knows how it will defeat it.

What this means in practice for landlords

For landlords already using these structures, or contemplating a move, the risk profile has changed materially.

Spotlight 63A makes it clear that HMRC has multiple, well-defined routes to challenge the outcome. This increases the likelihood of enquiries and significantly reduces the scope for defending the position if challenged.

In practical terms, this may lead to:

- Reallocation of profits back to the individual landlord

- Additional income tax liabilities

- Interest and penalties

- Unexpected charges, including SDLT

- Potential ongoing liabilities, such as ATED for certain structures

Many landlords entered into these arrangements in good faith, often based on professional advice. However, HMRC’s focus is on the effect of the structure, not the intention behind it.

For those considering similar arrangements today, the position is now clear. This is not an emerging risk – it is an area where HMRC has already formed and published a detailed view.

A familiar pattern in the property sector

For landlords and property investors, there is a broader pattern here that is worth recognising.

Since the restriction of mortgage interest relief, landlords have been presented with a range of strategies designed to reduce their tax exposure. Some are entirely appropriate when aligned with a genuine commercial structure. Others rely on recharacterising income without any meaningful change in how the business operates.

HMRC’s response has been consistent. Where the structure does not reflect the underlying reality, it will be challenged.

The cycle is familiar: a solution is marketed, it gains traction, HMRC reviews it, and eventually publishes its position. By that point, many landlords are already committed.

The way forward: taking control early

If any of this feels familiar, the most important step is to review your position early and take the appropriate action.

Structures involving LLPs with corporate members, particularly those established in response to mortgage interest relief changes, remain a clear area of focus. The addition of indemnity-based arrangements only increases the need for a detailed review.

Acting early preserves options and, depending on the circumstances, this may involve restructuring, engaging with HMRC proactively, or planning an orderly exit from the arrangement.

Waiting reduces those options – often significantly – and can increase both the financial and administrative cost of resolving the position.

How can we help

At Wilkins Southworth, we have supported a growing number of landlords affected by Spotlight 63 and similar arrangements.

Our focus is on how the structure operates in practice, not just how it was intended to work. This allows us to assess the level of exposure and identify the most effective route forward.

Where HMRC engagement is required, we assist with managing enquiries, negotiating outcomes and, where possible, reducing penalties. In other cases, the priority is restructuring and ensuring future arrangements are aligned with both commercial objectives and current tax rules.

Each situation is different, but early engagement typically leads to more flexibility and better outcomes.

Final thoughts

Spotlight 63A is not a standalone update. It is the continuation of a process that has been developing over several years and is now becoming more definitive.

HMRC has moved beyond general warnings and is now setting out in detail why these arrangements fail and how they will be challenged.

For landlords, this is no longer a question of interpretation, but more one of understanding your position and deciding what to do next. If you are unsure about your current structure or concerned about potential exposure, now is the time to get in touch so we can assess your current situation.