HMRC Reasonable Care

Most people assume that once they've appointed an accountant, responsibility for preparing an accurate tax return passes to them.

Parker v HMRC

Most people assume tax residence disputes revolve around complex planning structures or aggressive tax strategies.

Foreign Income and Gains

For many internationally mobile individuals, the abolition of the remittance basis and introduction of the Foreign Income and Gains (FIG) regime initially sounded relatively attractive.

HMRC’s Referee Defeat

After almost a decade in the courts, HMRC has again lost its employment status case against football referees engaged by PGMOL.

Reasonable Care and Carelessness

Wilkins Southworth won the argument when HMRC penalised a client for inaccuracies in a filing by their previous accountant.

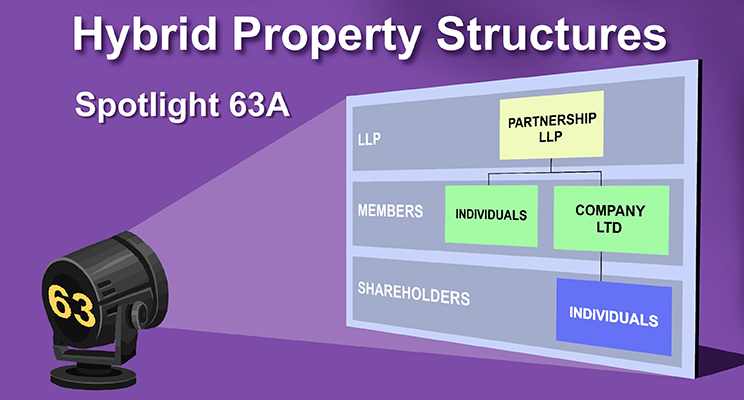

Spotlight 63A

Many landlords assumed the conversation around hybrid LLP structures had run its course following HMRC’s original Spotlight 63.

When a Tax Refund Isn’t What It Seems

For most people, a tax refund is straightforward: an overpayment is corrected, a missed expense is claimed, and the money comes back.

HMRC’s New Reporting Rules

HMRC’s focus on small businesses is shifting again, and this time, it’s not about what you earn, but how money moves between you and your company.

HMRC Financial Institution Notices

HMRC’s information-gathering powers have evolved, and one tool in particular is worth understanding.

- 1

- 2

- 3

- 4

- …

- 12

- Go to the next page